All Categories

Featured

Table of Contents

The are entire life insurance coverage and global life insurance policy. The cash money value is not included to the fatality advantage.

After 10 years, the cash money value has actually expanded to around $150,000. He obtains a tax-free financing of $50,000 to start a service with his bro. The policy financing passion price is 6%. He settles the financing over the following 5 years. Going this course, the interest he pays returns right into his plan's cash money value rather than a banks.

Concept Bank

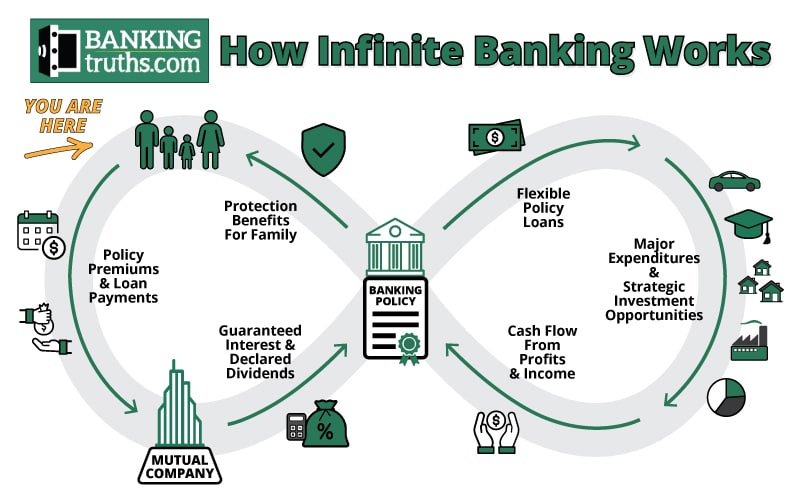

The concept of Infinite Financial was created by Nelson Nash in the 1980s. Nash was a finance specialist and fan of the Austrian college of business economics, which promotes that the value of goods aren't clearly the outcome of conventional economic structures like supply and demand. Instead, people value money and products in a different way based on their economic standing and demands.

Among the challenges of typical financial, according to Nash, was high-interest prices on financings. Way too many people, himself consisted of, entered financial trouble because of dependence on financial organizations. As long as financial institutions set the rate of interest and funding terms, people didn't have control over their very own wide range. Becoming your own banker, Nash figured out, would put you in control over your economic future.

Infinite Financial needs you to have your financial future. For ambitious individuals, it can be the very best economic tool ever before. Below are the benefits of Infinite Financial: Arguably the solitary most helpful facet of Infinite Financial is that it enhances your cash flow. You do not require to go with the hoops of a conventional bank to get a financing; merely request a plan funding from your life insurance policy firm and funds will certainly be made available to you.

Dividend-paying whole life insurance policy is extremely reduced risk and offers you, the policyholder, a fantastic bargain of control. The control that Infinite Financial supplies can best be grouped right into two groups: tax obligation benefits and property securities - infinite wealth and income strategy. One of the reasons whole life insurance policy is optimal for Infinite Banking is just how it's taxed.

Infinite Family Banking

When you utilize whole life insurance policy for Infinite Financial, you get in into a personal agreement between you and your insurance firm. This privacy offers certain asset defenses not discovered in other monetary cars. These defenses might vary from state to state, they can include security from asset searches and seizures, protection from judgements and defense from financial institutions.

Entire life insurance policies are non-correlated properties. This is why they work so well as the economic foundation of Infinite Financial. Regardless of what takes place in the market (supply, genuine estate, or otherwise), your insurance coverage plan keeps its worth.

Entire life insurance coverage is that third container. Not only is the rate of return on your entire life insurance coverage policy ensured, your death advantage and costs are additionally guaranteed.

This structure straightens perfectly with the principles of the Perpetual Riches Approach. Infinite Banking appeals to those seeking greater economic control. Below are its primary benefits: Liquidity and access: Plan lendings supply prompt accessibility to funds without the limitations of traditional bank fundings. Tax obligation efficiency: The cash money value expands tax-deferred, and policy finances are tax-free, making it a tax-efficient device for developing riches.

Infinite Banking Concept Uk

Asset security: In several states, the cash money value of life insurance policy is secured from creditors, including an extra layer of financial security. While Infinite Financial has its merits, it isn't a one-size-fits-all option, and it features substantial disadvantages. Below's why it may not be the finest method: Infinite Financial usually needs complex policy structuring, which can confuse policyholders.

Visualize never ever needing to stress over small business loan or high rate of interest once again. What if you could borrow cash on your terms and construct wealth all at once? That's the power of infinite financial life insurance. By leveraging the cash worth of whole life insurance IUL plans, you can grow your wealth and borrow cash without counting on traditional banks.

There's no set car loan term, and you have the liberty to choose the settlement timetable, which can be as leisurely as paying back the lending at the time of death. This versatility extends to the servicing of the lendings, where you can go with interest-only payments, maintaining the finance equilibrium level and convenient.

Holding cash in an IUL fixed account being credited rate of interest can commonly be far better than holding the money on down payment at a bank.: You have actually constantly fantasized of opening your own pastry shop. You can obtain from your IUL policy to cover the preliminary costs of renting a room, acquiring tools, and employing team.

Bank Infinity

Personal lendings can be acquired from standard banks and credit score unions. Obtaining cash on a credit scores card is typically very expensive with yearly percentage prices of interest (APR) typically getting to 20% to 30% or more a year.

The tax therapy of policy finances can vary substantially relying on your country of house and the details terms of your IUL policy. In some areas, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, policy lendings are normally tax-free, offering a considerable advantage. Nevertheless, in various other territories, there may be tax obligation effects to take into consideration, such as prospective taxes on the funding.

Term life insurance coverage only supplies a survivor benefit, without any type of cash worth accumulation. This means there's no cash worth to borrow against. This write-up is authored by Carlton Crabbe, President of Capital permanently, a specialist in supplying indexed global life insurance policy accounts. The info provided in this write-up is for instructional and informational functions only and ought to not be understood as economic or investment recommendations.

However, for loan officers, the substantial laws enforced by the CFPB can be viewed as cumbersome and limiting. Initially, financing police officers often say that the CFPB's regulations produce unnecessary bureaucracy, leading to even more paperwork and slower funding handling. Rules like the TILA-RESPA Integrated Disclosure (TRID) policy and the Ability-to-Repay (ATR) requirements, while intended at safeguarding customers, can bring about delays in closing bargains and increased functional prices.

{kind=link}

Latest Posts

Ibc Whole Life Insurance

Allan Roth Bank On Yourself

Becoming Your Own Banker And Farming Without The Bank