All Categories

Featured

Table of Contents

Okay, to be fair you're really "banking with an insurance provider" as opposed to "financial on yourself", however that concept is not as easy to offer. Why the term "infinite" financial? The concept is to have your money operating in several areas at the same time, instead than in a single area. It's a little bit like the idea of acquiring a house with cash, after that borrowing against your house and putting the cash to work in one more financial investment.

Some people like to speak regarding the "rate of money", which primarily means the exact same thing. That does not mean there is absolutely nothing worthwhile to this idea once you get past the marketing.

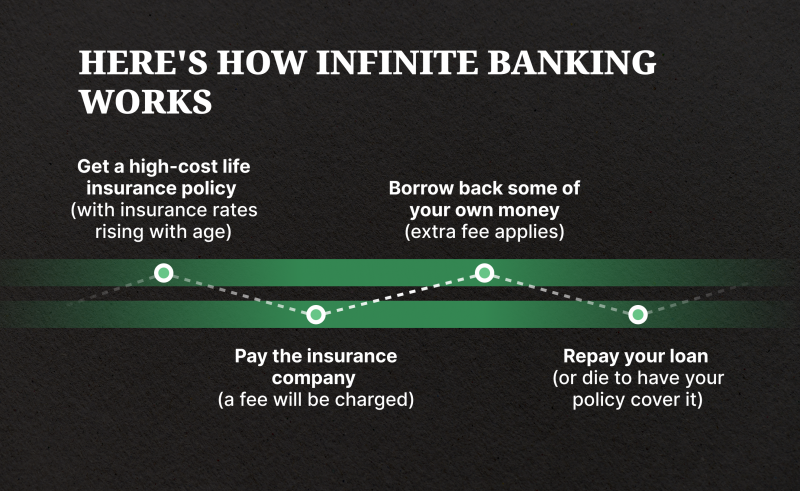

The entire life insurance policy sector is plagued by excessively expensive insurance policy, large commissions, unethical sales methods, reduced prices of return, and improperly informed clients and salesmen. However if you desire to "Bank on Yourself", you're going to have to fall to this sector and in fact get entire life insurance policy. There is no substitute.

The assurances integral in this item are essential to its function. You can obtain versus the majority of sorts of cash money worth life insurance policy, however you shouldn't "financial institution" with them. As you acquire a whole life insurance coverage policy to "financial institution" with, keep in mind that this is an entirely separate section of your economic plan from the life insurance coverage section.

As you will see below, your "Infinite Financial" plan truly is not going to dependably supply this vital financial function. One more trouble with the fact that IB/BOY/LEAP relies, at its core, on a whole life policy is that it can make purchasing a plan bothersome for many of those interested in doing so.

Visa Infinite Alliance Bank

Hazardous pastimes such as diving, rock climbing, sky diving, or flying likewise do not mix well with life insurance policy products. The IB/BOY/LEAP advocates (salesmen?) have a workaround for youbuy the plan on a person else! That might work out fine, given that the factor of the plan is not the survivor benefit, but remember that acquiring a policy on minor youngsters is much more pricey than it needs to be since they are usually underwritten at a "typical" price instead of a liked one.

Most plans are structured to do either points. The majority of frequently, policies are structured to optimize the payment to the agent selling it. Cynical? Yes. It's the fact. The commission on an entire life insurance policy policy is 50-110% of the first year's premium. Often plans are structured to make best use of the fatality advantage for the premiums paid.

The price of return on the policy is extremely essential. One of the best methods to maximize that factor is to get as much cash as possible into the plan.

The very best way to boost the rate of return of a policy is to have a fairly tiny "base plan", and afterwards placed more cash money right into it with "paid-up enhancements". Rather of asking "Just how little can I put in to get a particular survivor benefit?" the concern ends up being "Just how much can I lawfully took into the policy?" With more money in the plan, there is even more money value left after the prices of the fatality benefit are paid.

An extra advantage of a paid-up enhancement over a regular premium is that the payment price is lower (like 3-4% instead of 50-110%) on paid-up additions than the base policy. The much less you pay in commission, the greater your rate of return. The price of return on your cash money value is still going to be unfavorable for a while, like all cash money value insurance coverage.

Most insurance business just provide "straight acknowledgment" fundings. With a straight recognition financing, if you borrow out $50K, the reward price applied to the cash money value each year only applies to the $150K left in the plan.

Rbc Infinite Private Banking

With a non-direct acknowledgment loan, the business still pays the exact same reward, whether you have actually "borrowed the cash out" (technically versus) the policy or not. Crazy? That understands?

The business do not have a resource of magic complimentary money, so what they give up one place in the policy need to be extracted from another location. If it is taken from a feature you care much less about and place right into a feature you care more about, that is a great point for you.

There is one more essential attribute, typically called "laundry loans". While it is excellent to still have actually dividends paid on cash you have actually taken out of the policy, you still need to pay passion on that finance. If the returns price is 4% and the finance is charging 8%, you're not specifically appearing ahead.

With a wash car loan, your funding rate of interest is the very same as the dividend rate on the policy. So while you are paying 5% passion on the funding, that rate of interest is totally balanced out by the 5% returns on the car loan. In that regard, it acts just like you took out the cash from a financial institution account.

5%-5% = 0%-0%. Same very same. Therefore, you are now "financial on yourself." Without all 3 of these variables, this policy just is not mosting likely to work extremely well for IB/BOY/LEAP. The most significant problem with IB/BOY/LEAP is the people pushing it. Almost all of them stand to make money from you purchasing into this principle.

There are many insurance coverage representatives speaking regarding IB/BOY/LEAP as an attribute of entire life that are not in fact selling policies with the necessary attributes to do it! The problem is that those that understand the principle best have a large conflict of rate of interest and usually inflate the advantages of the principle (and the underlying plan).

Specially Designed Life Insurance

You should compare loaning versus your plan to withdrawing money from your cost savings account. No money in cash value life insurance policy. You can place the money in the financial institution, you can invest it, or you can purchase an IB/BOY/LEAP plan.

You pay taxes on the interest each year. You can conserve some more money and placed it back in the banking account to start to earn interest again.

It grows for many years with funding gains, returns, leas, and so on. A few of that earnings is exhausted as you accompany. When it comes time to acquire the boat, you sell the investment and pay taxes on your long-term resources gains. After that you can save some more cash and get some even more financial investments.

The money value not made use of to pay for insurance policy and compensations expands over the years at the reward price without tax drag. It begins with unfavorable returns, however hopefully by year 5 or so has recovered cost and is growing at the reward price. When you most likely to buy the boat, you obtain against the plan tax-free.

The Infinite Banking System

As you pay it back, the cash you repaid begins expanding again at the returns price. Those all job quite in a similar way and you can contrast the after-tax rates of return. The 4th alternative, nevertheless, works really in a different way. You do not save any type of cash neither buy any kind of type of investment for many years.

They run your credit scores and provide you a lending. You pay interest on the borrowed money to the bank until the funding is paid off.

{kind=link}

Latest Posts

Ibc Whole Life Insurance

Allan Roth Bank On Yourself

Becoming Your Own Banker And Farming Without The Bank